In the previous article – “The new mobility paradigm: evolving consumer needs and technologies” – the main trends that are being observed in society were identified, in particular relating to the new consumption habits of the generations, demographic trends and the increasing digitalisation of society. This part was accompanied by one dedicated to eight technologies – Vehicle Connectivity, User & Vehicle Data, Human Machine Interface, Marketplace, Connected Services, Sharing service, Autonomous Driving and Digital Platforms – which enable new applications in the sphere of connected mobility that were unthinkable a few years ago.

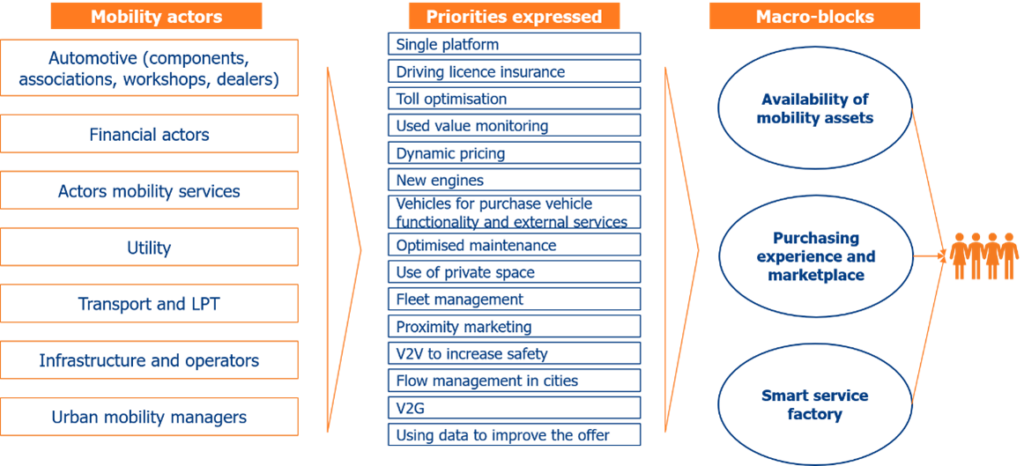

In this article we give a high-profile view of the evolutionary model of mobility envisaged by OCTO and The European House – Ambrosetti. The strategic vision is the result of the analyses carried out following the ideas that emerged from the thematic workshops held in March. More than 30 executives from 7 different industries/sectors took part in these meetings: automotive, finance, mobility services, utilities, transport and LPT, infrastructures and managers, urban mobility actors.

The speeches made by the players involved identified the main issues that will characterise the mobility of the future; to name but a few: the creation of a Mobility-as-a-Service model as an integration of the various mobility offers; the increasing commoditisation of the vehicle; the importance of micro-mobility as an integration of urban mobility; the increasing dematerialisation of the consumer experience; the evolution of the contact points between user and infrastructure and proximity marketing (e.g. service stations; the importance of communication standards between vehicles and between vehicles and infrastructure (V2V and V2X)); the potential of machine learning; the integration of vehicles in energy systems (V2V and V2X); the potential of machine learning; the integration of vehicles in energy systems (V2V and V2X). (e.g. petrol stations); the importance of communication standards between vehicles and between vehicles and the infrastructure (V2V and V2X); the potential of machine learning; the integration of vehicles into energy systems (V2Grid).

These arguments and points for reflection have been elaborated by The European House – Ambrosetti Working Group in order to develop a vision of the customer centric mobility ecosystem: as has already happened in other industries, for example the financial one, business models will have to keep customers increasingly in mind and focus the value proposition on the creation of a complete and satisfying consumer experience.

Adopting a customer-centric point of view, The European House – Ambrosetti has identified three macro-blocks at the basis of the future mobility ecosystem:

- Availability of mobility assets – access to different types of vehicles and vehicles, management of vehicle maintenance, availability of space, ease of refuelling and recharging.

- Buying experience and marketplace – simplicity of customer interface, aggregation, offer and sale of mobility services per user, offer and sale of smart services.

- Smart service factory – availability of smart services for drivers, cities and fleet managers.

Each macro-block consists of a series of added value services that could enrich the mobility and travel experience. Just to mention a few examples: the possibility of choosing different forms of mobility based on needs, even in aggregate form; platforms as enablers of new forms of supply and services in an integrated way; improving city mobility management, flows and spaces, LPT flexibility, air quality and road maintenance through the use of data.

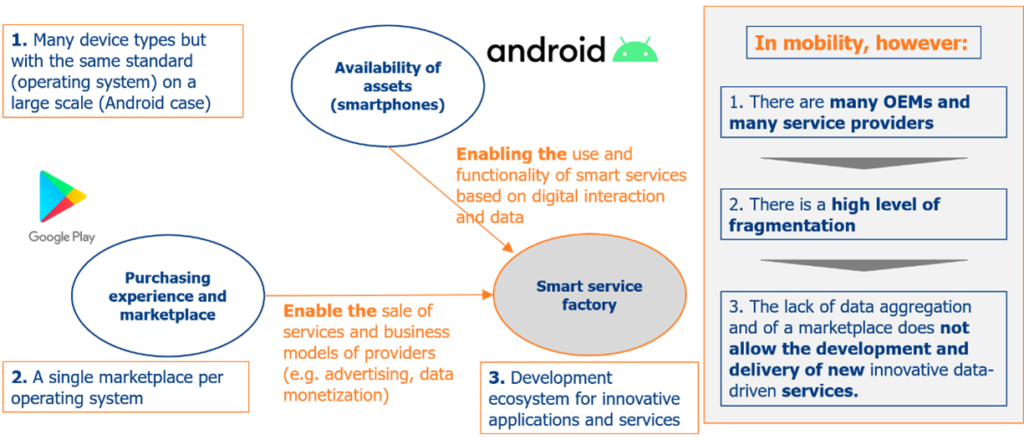

At the intersection of the three macro-blocks, a new model of mobility is identified, defined as Mobility-as-a-Service – i.e. mobility whose services are all within the reach of smartphones -, based on the optimisation of the user experience, enriched by the interaction between the different components of the ecosystem, and on alignment with Vision Zero (Zero Crash, Zero Traffic, Zero Pollution) – described in the previous article in this series.

To enable this new mobility model, two key elements need to be promoted and stimulated within the various mobility stakeholders: firstly, the importance of data and the need for openness, and secondly, the adoption of the platform model and the opportunity for co-opetition.

When combined, asset availability, marketplace and smart service factory create a new customer centric mobility ecosystem capable of generating more value than optimising individual businesses.

The parallelism with the world of telephony is evident: already in smartphones, there are examples of players that have benefited greatly from the development of an ecosystem model that includes a series of value-added services, the apps, delivered to customers through a single marketplace platform. The creation of an ecosystem where synergies can be developed between the different players in the value chain has favored for some players, for example Apple and Android, the achievement of a large scale of customers and partners for the development of services.

On the contrary, in the automotive world many OEMs and Service Providers operate in a fragmented way, limiting their operations to only those activities that are essential for ordinary business development, without adopting an ecosystem view. As a result, the lack of data aggregation and a marketplace does not allow the development and delivery of innovative services based on analytics of data collected from customers, vehicles and connected infrastructure.

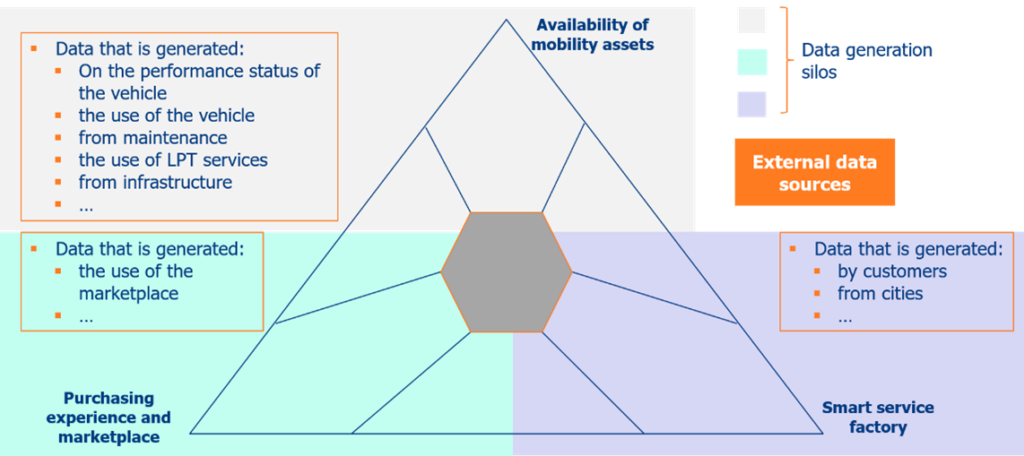

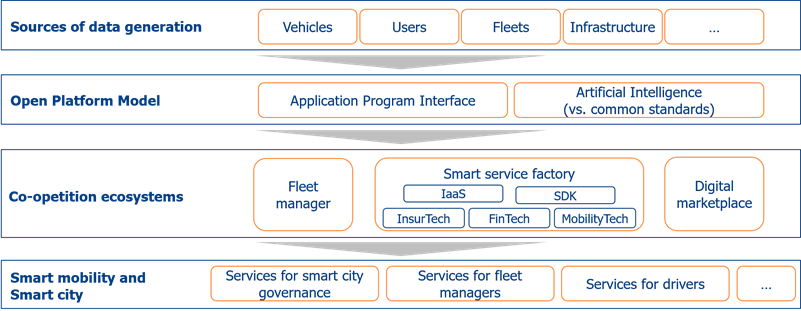

Within the mobility ecosystem there is a large number of sources of data generation. In each of the different subdivisions of the model developed by The European House – Ambrosetti there are players that contribute directly and/or indirectly to their generation. To date, however, the fragmentation of players and the impossibility of aggregating data, generated within the silos of each company in the supply chain, makes it difficult to create new value outside the optimisation of individual businesses.

On the contrary, the evolution of the mobility model towards an increasingly connected ecosystem, in which different players collaborate to create an all-inclusive offer to be conveyed to customers, requires an evolution of the relational logics between the different market players. Collaboration, data exchange and the use of data sources outside the restricted mobility ecosystem would allow the development of new offers and new business models based on the processing of collected data.

According to the vision of The European House – Ambrosetti, the creation of a connected ecosystem of data sharing from different sources and systems can be enabled by the use of a platform business model, i.e. a connected ecosystem in which different players collaborate in order to offer an end-to-end customer experience. In this sense, data becomes the main asset of companies that want to operate within the ecosystem and its processing to improve the offer is one of the main areas in which to concentrate resources and investments.

The development of a platform ecosystem enables four main competitive advantages for participating actors:

- Platforms make it possible to improve the exchange of data in a logic of openness and sharing.

- Data sharing makes it possible to break down the traditional structure of value chains, leading to convergence between actors in different sectors.

- The coexistence of several actors (and sectors) allows to design and deliver an end-to-end experience to customers.

- Through platform logics it is possible to share assets (e.g. access to customers, technological infrastructures, Service Development Kits – SDKs) that increase the possibility of rapid introduction of innovations by large ecosystems of players (e.g. Fintech in the financial sector).

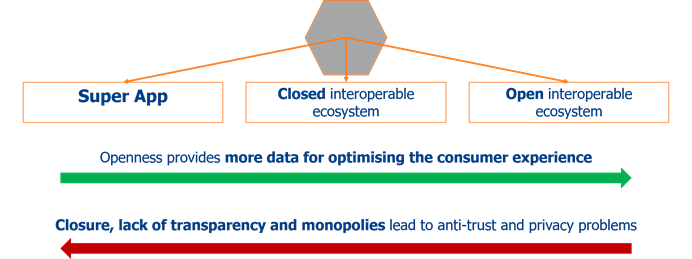

In terms of platform model configuration, The European House – Ambrosetti proposes three different alternatives:

- the first, called SuperApp, is an application that can offer a seamless, integrated, contextualised and efficient complete consumer experience. In this first case, the large user base and the unified management of the customer experience are considered value-generating advantages. At the same time, this model poses challenges regarding the proper management of competition and antitrust;

- the second model is defined as a closed interoperable ecosystem and involves collaboration between defined partners working in synergy to offer a range of services to customers. In this model, the objectives and purpose of the collaboration and the relationships between the companies are clear. There is also a high level of privacy management, guaranteed by defined security standards among the ecosystem actors. The weakness relates to the lack of dynamism of the model, due in particular to the lack of openness towards external partners;

- finally, there is the open interoperable ecosystem, a model that envisages collaboration between different players in the ecosystem according to a logic of co-opetition and co-creation of end-to-end services. In this case, the ecosystem players are configured according to a logic of flexibility and rapidity of action with high levels of innovation. A potential difficulty of this highly dynamic model is the management of market players, particularly in the initial stages.

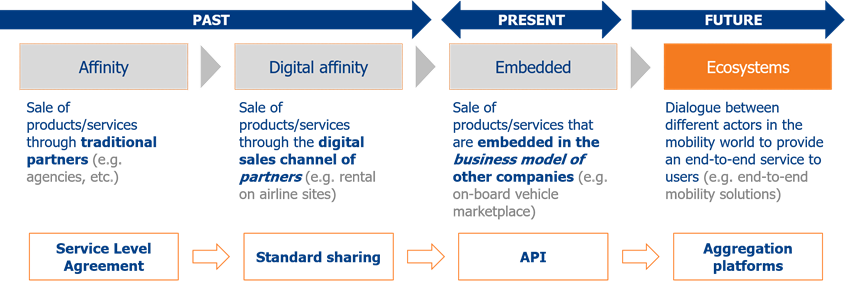

Concretely, with respect to the mobility ecosystem, we expect a model very similar to the third one described, i.e. an open interoperable model in which a large number of actors, belonging to different components of the value chain, collaborate to generate new offers and new experiential models for customers.

As described in the figure above, the different data sources will be connected thanks to API and AI systems. Once the datasets are created, the different actors will be able to use them to create new offers integrated within the connected ecosystem. The new products and services will then be conveyed to the market and can contribute to the realisation of the full value of smart mobility and smart cities.

Ultimately, it can be said that the possibility of creating a connected ecosystem, where different mobility actors contribute with different data sources, will enable new value for the different users of mobility services. In order to develop this model in practice, several challenges will have to be addressed, starting with the involvement of the actors of the value chain, the creation of the technological infrastructure and of standards for sharing. In the vision of OCTO and The European House – Ambrosetti, this ecosystem can be created starting from small project pilots developed in controlled environments, which will have the purpose of making the real potential of the model understood.

In the next article in this series, we will further develop the model proposed by The European House – Ambrosetti, defining project steps, actors to be involved, other needs and enabling elements with the aim of defining a real development timeline. These recommendations will be enriched by the results of the second block of three working tables that will take place in June.

Authors:

Alessandro Viviani : Senior Consultant – Innotech Hub

Corrado Panzeri : Associate Partner – Head of InnoTech Hub

The European House – Ambrosetti