According to the fDi Report 2023, Global greenfield investment trends, over the course of 2021, annual sales of electric vehicles (EVs) doubled to a new record of 6.6 million. While just 120,000 EVs were sold worldwide in 2012, more than 120,000 EVs were sold each week in 2021 according to the International Energy Agency.

Cross-border investment monitor fDi Markets has recorded a marked increase in the number of announced foreign direct investment (FDI) projects in the EV business. Despite a lull in investments during the first year of the Covid-19 pandemic, investment into these technologies have continued to increase since 2016, both in terms of project number and value.

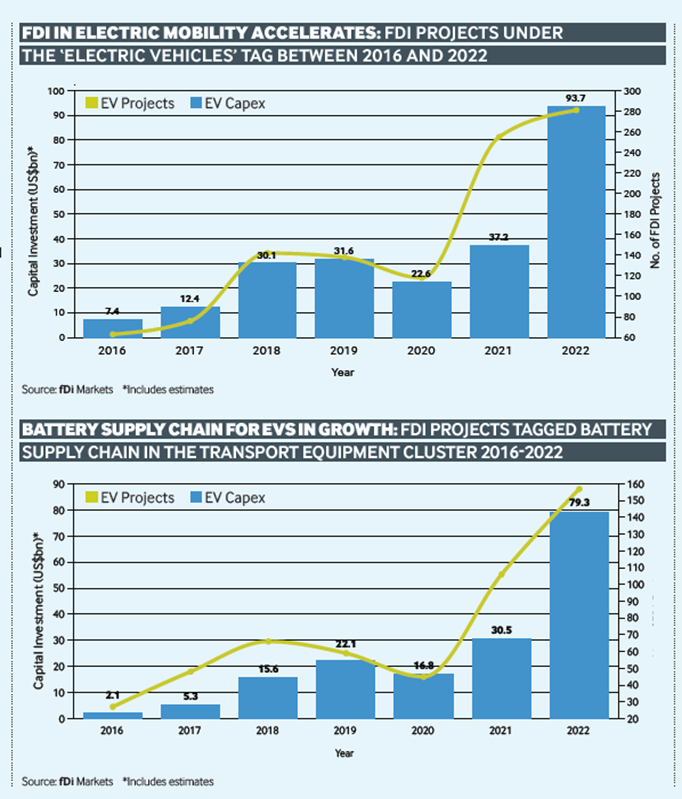

A total 281 FDI projects were recorded in 2022 with a cumulative value of $93.7bn — more than 1.5 times higher than in 2021 and nearly three times the capital investment announced in 2019. Manufacturing projects accounted for 96% of the capital investment and 54% of the announced FDI projects in 2022.

The investigation indicates that Tesla Motors was by far the most active investor in the area, with 59 FDI projects announced since 2016, including three big-ticket overseas gigafactories: Shanghai, Brandenburg and Monterrey.

While 2021 was a peak for Tesla, other automotive firms — both established and start-up companies — announced their highest number of EV projects during 2022. Vietnam’s new EV firm Vingroup announced more than $4.5bn in FDI projects in 2022 and traditional automakers such as Volkswagen, Daimler, BMW, Hyundai and Ford ramped up investments in EVs with a combined $25.1bn invested in 2022 alone.

As the cost of fuel continues to rise and the price gap between EVs and conventional cars decreases, EVs and hybrid vehicles are becoming an increasingly attractive choice for consumers. However, the study points out that there are several factors that are throttling uptake, including primarily their range. For EVs to be embraced in any significant way, the issue of how far they can travel between charges requires urgent investment and innovation.

While the range of these vehicles is increasing, wider access to charging points is needed to make charging EVs as easy as refueling internal combustion vehicles. McKinsey estimates that the EU 27 will need at least 3.4 million operational public charging points by 2030 to reach the target of becoming carbon-neutral by 2050 and to meet anticipated public demand.

The report indicates that alongside this, extensive energy grid upgrades will be required to distribute power to these new points. In all, McKinsey estimates this build-out of EV-charging infrastructure will cost more than €240bn by 2030.

Access to critical materials poses a risk

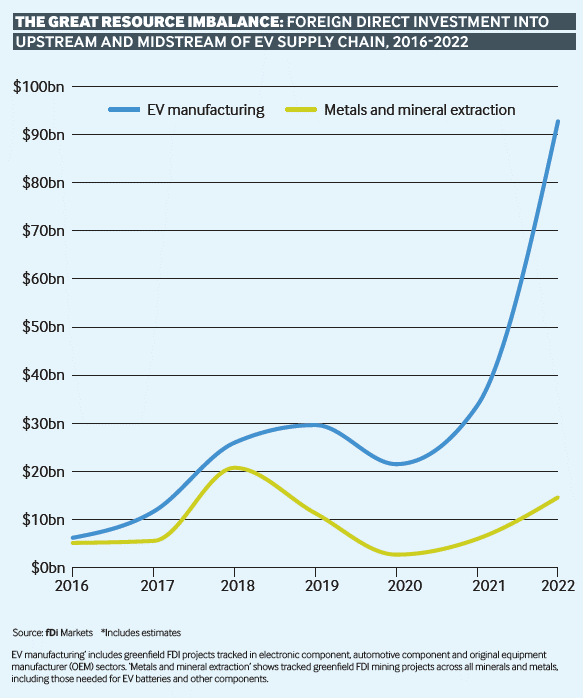

Battery innovations have driven up the average range of EVs from 127 km in 2010 to 349 km in 2021, according to IAE data. Despite the battery supply chain being fraught with critical material insecurity, suppliers appear to be making strategic early investments to ensure new factories are at nameplate capacity in time to meet the moment.

Markets have recorded an equally steep increase in the number of FDI projects tagged as part of the battery supply chain since 2016, as manufacturers are investing with future EV requirements in mind. When looking at only those projects serving the transport equipment cluster, we can see those investments totaling an estimated $79.3bn were announced in 2022, compared to just $22.1bn in 2019.

The research stress that because an EV battery can account for as much as 40% of the car’s cost and because the leading five battery makers hold an estimated 80% of the global market share according to Goldman Sachs research, battery supply chain constraints appear to have the most potential to slow growth in EV uptake as pricing power has shifted to the battery makers and limits profitability for automakers.

Investment outlook

According to the report, there is an uncertain outlook for EVs in the near-term, but companies appear undeterred and continue to invest in electrification, spurred on by mounting incentives and policy support — from the Inflation Reduction Act in the US to the EU’s Green Deal Industrial Plan.

This pressure has brought about advances in electrifying light commercial vehicles (LCVs) fleets globally. LCVs are particularly ripe for investment as many are used for urban delivery and since LCV fleets are driven intensively, often operate on predictable routes and can be charged at commercial depots.

Electric medium- and heavy-duty truck sales totaled more than 14,200 in 2021, which represents less than 0.3% of the total number of registrations for such vehicles worldwide and as such, this segment has growth potential — particularly in the electric bus space. The EU’s Clean Vehicles Directive has led to national targets to transition to public procurement of only zero-emission buses, and this will no doubt increase uptake.

In the LCV space, Saic Maxus Automotive, announced an ambitious strategy aiming to become the largest supplier in Europe, while UK-based truck firm Teeva Motors raised $54m to fund its North American and European expansion plan. Supporting technologies are also in receipt of funding for the implementation of existing technologies.

The investigation stresses that the climate for EVs is not without its challenges; however, there are no signs that demand from consumers will wane, and strong support exists from governmental organizations, so it is likely that investments in this space will continue to grow. Implications of the Inflation Reduction Act in the US as well as similar policies across the world do leave questions on how countries will compete for the market share in this lucrative industry.